Investing in India Post savings schemes is one of the safest ways to grow your money. Since these schemes are backed by the government, your capital is completely safe and your returns are guaranteed. However, life is unpredictable. A sudden medical emergency, home renovation, wedding, or business cash crunch can arise when you least expect it.

When faced with a sudden need for cash, many people make the mistake of breaking their long-term investments early. Doing this usually triggers heavy penalty charges, involves tedious paperwork, and permanently stops your compounding interest benefits.

Fortunately, there is a much smarter option. You can get a secured loan by using your savings certificates as collateral, keeping your investment intact.

This guide explains how borrowing against Post Office investments works, who can apply, and the mistakes you must avoid.

The Truth About “Policybazaar Post Office Loans”

If you have been researching this online, you might have seen terms like “Policybazaar Post Office Loan.” Let us clear up this common misunderstanding right away.

Policybazaar does not offer or manage loans against Post Office savings.

Policybazaar is simply an online financial marketplace. It helps you compare standard credit products—like personal loans, home loans, or business loans—offered by different banks and non-banking financial companies (NBFCs).

You cannot apply for a Post Office loan on Policybazaar. However, you can use the platform to compare standard personal loan rates against the secured rates offered by banks. To get a loan using your government savings certificates, you must apply directly to a participating bank and coordinate the official pledging process with India Post.

How Does a Loan Against Policy Bazaar Post Office Investment Work?

A loan against a savings certificate is a simple secured loan. Instead of breaking your investment and stopping its growth, you temporarily hand over the legal rights of your savings to a bank.

Here is how the process works:

- The Collateral: You submit your physical or electronic Post Office certificates to a bank.

- The Lien (Hold): The bank places a legal hold (called a “lien”) on your certificates. The Post Office branch where your account is registered will officially record this hold.

- Uninterrupted Growth: While your certificates are locked, your money remains completely safe. It continues to earn interest at the exact government rate fixed on the day you bought them.

- The Settlement: Once you repay the loan principal and interest in full through your monthly EMIs, the bank removes the hold, and you get full ownership of your certificates back.

Which Post Office Schemes Are Eligible for Loans?

The Government of India runs many small savings schemes, but banks do not accept all of them. Lenders only want collateral that they can easily value, officially transfer, and sell if a borrower defaults.

1. National Savings Certificate (NSC)

The NSC is the most widely accepted Post Office document for securing bank loans. Because NSCs have a fixed 5-year maturity period and a clear face value, banks view them as low-risk collateral. Pledging an NSC is a quick and smooth process at most major banks.

2. Kisan Vikas Patra (KVP)

KVP is another popular choice for investors because it promises to double the initial investment over a specific period. Like the NSC, you can officially transfer and pledge KVP certificates to commercial banks or cooperative societies as security for a loan.

3. Public Provident Fund (PPF)

The PPF is a highly restricted account. You cannot pledge a PPF account to a commercial bank for a standard retail loan. However, the Post Office itself offers a special, limited loan facility against your PPF balance. This option is only available between the third and sixth financial years of opening the account, and the loan amount is capped at 25% of the balance available at the end of the second preceding year.

4. Non-Eligible Schemes

Schemes like Sukanya Samriddhi Yojana (SSY), Senior Citizens Savings Scheme (SCSS), and the Monthly Income Scheme (MIS) have strict welfare rules or specific payout structures. Because of their legal design, you cannot pledge these accounts as collateral to banks.

Step-by-Step Guide to the Application Process

Getting a loan against your savings certificates requires coordination between the bank and India Post. Follow these four steps to apply:

Step 1: Check Bank Acceptance

Not all banks accept certificates from every single Post Office location. Your first step is to visit your preferred bank (like SBI, PNB, or major private banks) to confirm they will accept your specific certificates.

Step 2: Submit Your Application

Give the bank copies of your identity documents along with the original physical or electronic copies of your NSC or KVP certificates. The bank will calculate the current value of your certificates, checking the initial purchase amount and the interest earned up to that day.

Step 3: Complete Post Office Transfer Formalities

Once the bank gives you conditional approval, visit the Post Office branch where your certificates are registered. Submit a formal application for transfer (Form NC-41 or equivalent) to authorize the Post Office to register the bank as the official pledgee. The Post Office will stamp the certificates or issue an electronic note confirming the legal hold.

Step 4: Receive Your Funds

Take the officially stamped certificates back to your bank. The bank will store the documents safely in their vault, complete the remaining loan paperwork, and transfer the loan money directly into your savings account.

Eligibility and Documentation Checklist

Even though the loan is backed by your investment, banks must follow regulations to ensure you can repay the debt.

Who Can Apply?

- Age: You must generally be at least 18 years old to apply, and no older than 60 to 65 years by the time the loan ends.

- Employment: Banks prefer salaried individuals, self-employed professionals, and registered business owners who have a steady income to pay regular monthly EMIs.

- Credit Score: Lenders will check your credit report to see how you handled past payments. A minor drop in your credit score will not usually ruin a secured application, but active defaults or write-offs can cause a bank to reject it.

Required Documents

Gather these items before you apply to ensure fast processing:

- Identity Proof: Valid passport, voter ID card, or driver’s license.

- Address Proof: Recent utility bills (electricity or water), a registered rent agreement, or a bank statement showing your current address.

- PAN Card: Mandatory for tax compliance and credit checks in India.

- Original Certificates: Physical NSC or KVP papers, or clear printouts of verified e-certificates.

- Income Proof: Salary slips, bank statements from the last 3 to 6 months, or filed Income Tax Returns (ITR) to prove you can afford the EMIs.

- Photographs: Two to four recent passport-sized color photos.

Interest Rates and Loan Limits

Understanding the costs of a secured loan helps you get a fair deal. Since these loans are backed by the government, they carry very low risk for lenders.

How Much Can You Borrow? (LTV Ratio)

Banks never lend you 100% of your investment’s value. Instead, they keep a safety buffer called the Loan-to-Value (LTV) ratio. For NSC and KVP investments, banks typically offer a loan amount ranging between 70% and 90% of the asset’s current worth.

The bank decides this percentage based on either the initial face value or the current value including accumulated interest. The closer your certificate is to its final maturity date, the higher the loan amount the bank will likely approve.

Interest Rate Calculations

Because these loans are safe for lenders, their interest rates are much lower than standard personal loans. While an unsecured personal loan might charge interest rates from 12% to 24%, a loan secured by an NSC or KVP usually costs just 1.5% to 4% above the bank’s base rate or the internal interest rate of the savings scheme itself (typically in the 9% to 11% range).

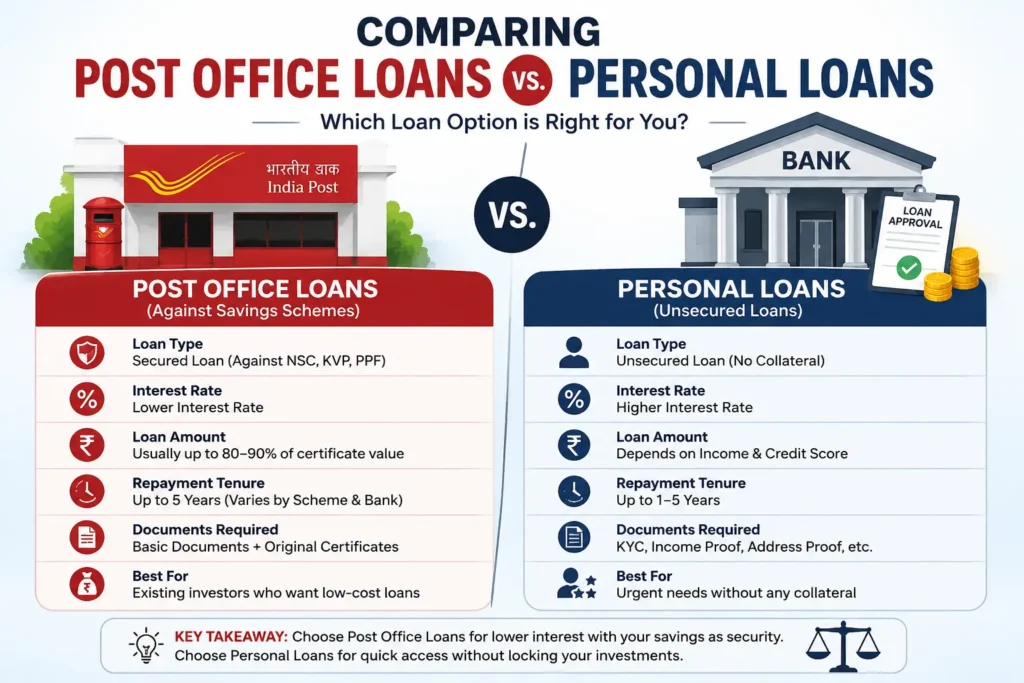

Comparing Post Office Loans vs. Personal Loans

Choosing the right type of debt depends on your financial situation. This table shows how a loan against your savings certificates compares to a standard personal loan.

| Feature | Loan Against Post Office Certificate | Standard Unsecured Personal Loan |

| Interest Rate | Lower (often in the 9% to 11% range) | Higher (typically 11% to 24% based on risk) |

| Collateral Required | Yes (NSC or KVP certificates) | No collateral or asset backing required |

| Impact on Savings | Savings stay intact and keep compounding | No direct impact on existing savings accounts |

| Processing Speed | Moderate (requires Post Office verification) | Fast (often instant or within 24–48 hours) |

| Maximum Loan Cap | Capped by the current value of the asset | Determined entirely by your salary and income size |

| Credit Score Impact | Less sensitive to minor credit flaws | Highly dependent on an excellent credit score |

Pros and Cons to Consider

Before locking your savings certificates away in a bank vault, weigh the benefits against the risks.

The Advantages

- Wealth Protection: Your investments stay active. If your certificate earns 7% annually, it keeps compounding at that exact pace throughout the entire life of your loan.

- Lower Costs: The lower interest rate means smaller monthly EMIs and less total interest paid over time.

- Financial Discipline: Pledging an asset forces you to pay off the debt systematically out of your monthly income rather than draining your hard-earned net worth.

The Risks

- Asset Loss: If you run into severe cash flow issues and default on your loan payments, the bank has the legal right to seize your certificates, cash them out at the Policy bazaar Post Office, and use the money to cover your debt.

- Locked Liquidity: Once you pledge a certificate, it is locked. If you face a bigger emergency a few months later, you cannot cash out that NSC or KVP early because of the bank’s legal hold.

Critical Factors to Double-Check Before Pledging

Never sign a loan agreement without reading the fine print. Ask the bank’s loan officer these questions first:

- What are the hidden fees? Look closely at processing fees, document verification charges, and valuation costs. High upfront fees can easily wipe out the savings from a lower interest rate.

- Are there prepayment penalties? If you receive a bonus or inheritance, you might want to pay off your loan early. Make sure the lender does not charge foreclosure or prepayment penalties for clearing your debt ahead of schedule.

- How often is the interest calculated? Find out if the interest is calculated on a monthly reducing balance or a daily reducing basis, as this changes your total cost over time.

Frequently Asked Questions (FAQs)

No. Policybazaar is an online comparison platform. It does not issue loans against Post Office savings schemes. You can use it to compare standard personal loans from different banks, but to get a loan against your government certificates, you must apply directly to a participating bank and set up the hold with India Post.

No, commercial banks cannot place a hold or take security over a PPF account. If you need a loan against your PPF balance, you must apply directly through the specific Post Office branch or bank where your PPF account is active. This facility is subject to strict timelines (between the 3rd and 6th fiscal years) and borrowing caps.

Yes. Your National Savings Certificate (NSC) or Kisan Vikas Patra (KVP) remains an active investment while locked in the bank’s vault. It will continue to earn interest and compound at the exact rate specified on the day you bought it. The bank’s hold simply prevents you from withdrawing the money until your debt is fully paid off.

If you default on your loan, the bank will first send you legal notices demanding payment. If you continue to default, the lender will use its legal rights to take full ownership of your pledged certificates. The bank will present the documents to India Post to cash them out and recover the unpaid loan balance. Any remaining money will be returned to your account.

The loan amount depends on the bank’s Loan-to-Value (LTV) limits, which typically run between 70% and 90% of the certificate’s eligible value. Banks calculate this value based on either the original face value or the accumulated value (face value plus earned interest) up to the day you apply.

Yes, most institutional banks still run a standard credit check during the application process. Even though the loan is fully secured by your investment certificates, banks check your credit score to evaluate your financial discipline and ensure you have a regular income to pay the monthly EMIs.

No. The Sukanya Samriddhi Yojana is a specialized social welfare initiative designed exclusively for the benefit of a girl child. Government regulations strictly prohibit ownership transfers or commercial holds on an SSY account, meaning you cannot use it as collateral for any bank loan.