Buying a home is one of the biggest financial goals for many people. However, before applying for a housing loan, most people want to know How much home loan can I get on ₹40,000 salary. The answer depends on several factors such as monthly income, credit score, existing financial commitments, age, employment stability, loan tenure, and the bank’s lending policies.

A person earning ₹40,000 per month can become eligible for a home loan if they meet the required criteria set by financial institutions. Banks generally evaluate the borrower’s repayment capacity before approving a loan amount. They analyze how much EMI a person can comfortably pay every month without affecting their daily expenses.

The increasing demand for affordable housing has made home loans easily available in India. Different banks offer different home loan interest rates in India, and borrowers should compare rates, processing charges, and repayment terms before selecting a lender. Understanding loan eligibility, EMI calculation, and documentation requirements can help you make a better financial decision.

Understanding Home Loan on ₹40,000 Salary

A Home loan on 40000 salary is possible, but the approved amount depends on the applicant’s financial profile. Banks usually consider a percentage of monthly income as the maximum EMI repayment capacity. Generally, lenders prefer that your total EMI obligations should not exceed around 40%–50% of your monthly income.

For a salary of ₹40,000 per month:

- Monthly income: ₹40,000

- Estimated EMI capacity: Around ₹16,000–₹20,000

- Loan amount: Depends on interest rate and repayment tenure

For example, if a person chooses a longer repayment period, they may get a higher loan amount because the monthly EMI becomes lower. However, a longer tenure also increases the total interest paid over the loan period.

Before applying, borrowers can use a home loan calculator to estimate their expected EMI and understand their repayment ability. This helps in planning finances and choosing a suitable loan amount.

How Banks Calculate Home Loan Eligibility

Banks use different methods to determine whether an applicant qualifies for a home loan. The main purpose is to check whether the borrower can repay the loan comfortably.

Some major factors considered during calculation include:

1. Monthly Income

Income is the most important factor in determining loan eligibility. A higher income generally allows borrowers to qualify for a higher loan amount.

For a ₹40,000 monthly salary, banks will check:

- Net monthly income

- Salary structure

- Fixed and variable income

- Employment type

- Income stability

2. Existing Financial Obligations

If you already have other loans such as:

- Personal loan

- Car loan

- Credit card dues

then your home loan eligibility may decrease because your repayment capacity becomes lower.

Banks calculate your remaining income after deducting existing EMIs before deciding your eligible loan amount.

3. Credit Score

A good credit score plays an important role in home loan approval. Generally, a credit score of 750 or above is considered favorable by many lenders.

A strong credit history can help borrowers get:

- Faster approval

- Better interest rates

- Higher loan eligibility

Using Home Loan Eligibility Calculator

A home loan eligibility calculator is an online tool that helps borrowers estimate the approximate loan amount they may qualify for based on their income and financial details.

To use a loan eligibility calculator, you generally need to enter:

- Monthly income

- Existing EMI payments

- Loan tenure

- Interest rate

- Age

- Employment details

The calculator provides an estimated eligible loan amount. However, the final approval depends on the bank’s verification process.

Different banks have their own calculation methods. For example, people searching for home loan eligibility calculator ICICI or other bank-specific calculators can check their approximate eligibility before applying.

Importance of Home Loan Interest Rates in India

Interest rate is one of the most important factors when choosing a home loan. Even a small difference in interest rates can create a significant difference in the total repayment amount.

Home loan interest rates in India vary depending on:

- Bank policies

- Applicant’s credit score

- Loan amount

- Loan tenure

- Type of interest rate (fixed or floating)

Before selecting a lender, borrowers should compare different options and understand how interest rates affect their EMI.

For existing borrowers, documents like the HDFC home loan interest certificate can help track the interest paid during a financial year, especially for tax-related purposes.

Why EMI Calculation Is Important Before Taking a Home Loan

Before applying for a home loan, understanding your monthly EMI is extremely important. Many borrowers take loans without calculating whether they can manage the monthly repayment comfortably.

People often search for how to calculate home loan emi because EMI depends on three main factors:

- Loan amount

- Interest rate

- Loan tenure

The formula helps borrowers understand their monthly financial responsibility and avoid future repayment difficulties.

A canara bank home loan emi calculator or similar bank EMI calculator can provide an estimate of monthly payments before applying for a loan.

What Is Home Loan Pre Approval?

Home loan pre approval is a process where a bank evaluates your financial profile and gives an estimated loan approval before you finalize a property.

Benefits of pre approval include:

- Understanding your borrowing capacity

- Better property budget planning

- Faster loan processing after property selection

- Increased confidence while negotiating with sellers

However, pre approval does not mean the final loan disbursement is guaranteed. The property documents and legal verification are still required before final approval.

How Much Home Loan Can I Get on ₹40,000 Salary?

When planning to buy a home, the most common question is “How much home loan can I get on ₹40,000 salary?” The exact loan amount depends on various factors such as income, age, credit score, existing loans, interest rate, and repayment period.

Generally, banks calculate home loan eligibility by considering your monthly income and repayment capacity. Most lenders allow borrowers to use around 40%–50% of their monthly income for EMI payments.

For a person earning ₹40,000 per month:

- Monthly salary: ₹40,000

- Possible EMI capacity: Approximately ₹16,000–₹20,000

- Possible loan amount: Around ₹20 lakh to ₹35 lakh (depending on tenure, interest rate, and borrower profile)

The final approval amount may vary from bank to bank because every lender has different eligibility rules.

How Banks Calculate Home Loan Amount Based on Salary

Banks use multiple calculations to decide the maximum loan amount a person can receive. The main calculation is based on the borrower’s repayment ability.

For example:

Monthly Income: ₹40,000

Maximum EMI considered: ₹16,000 (40% of income)

Loan Tenure: 20 years

Interest Rate: 8% approximately

Based on these factors, the eligible loan amount can be calculated.

A borrower can use a home loan calculator to estimate the EMI and understand how much loan they can comfortably repay.

The calculator considers:

- Principal loan amount

- Interest rate

- Loan tenure

- Monthly income

Using a calculator before applying helps borrowers avoid choosing a loan amount that creates financial pressure.

How to Calculate Home Loan EMI?

Many borrowers search for how to calculate home loan emi because EMI planning is an important step before taking a loan.

The EMI calculation depends on three major factors:

1. Loan Amount

The higher the loan amount, the higher will be the monthly EMI.

Example:

- ₹20 lakh loan → Lower EMI

- ₹35 lakh loan → Higher EMI

2. Interest Rate

Interest rate directly affects the EMI amount. A lower interest rate reduces monthly payments and total interest cost.

The home loan interest rates in India depend on:

- Bank policies

- RBI guidelines

- Credit score

- Loan type

- Borrower profile

3. Loan Tenure

Loan tenure means the time period in which you repay the loan.

Longer tenure:

- Lower monthly EMI

- Higher total interest payment

Shorter tenure:

- Higher monthly EMI

- Lower total interest payment

A borrower should select a tenure according to their monthly budget.

Example of Home Loan EMI Calculation for ₹40,000 Salary

Suppose a person earning ₹40,000 salary takes a home loan:

Loan Amount: ₹25 lakh

Interest Rate: 8% per year

Loan Tenure: 20 years

Approximate EMI: Around ₹20,900 per month

In this situation, the borrower should check whether this EMI fits within their monthly expenses.

A person with additional financial responsibilities may choose a lower loan amount or longer tenure to maintain comfortable repayment.

Using a home loan eligibility calculator along with an EMI calculator can provide a clearer picture of affordability.

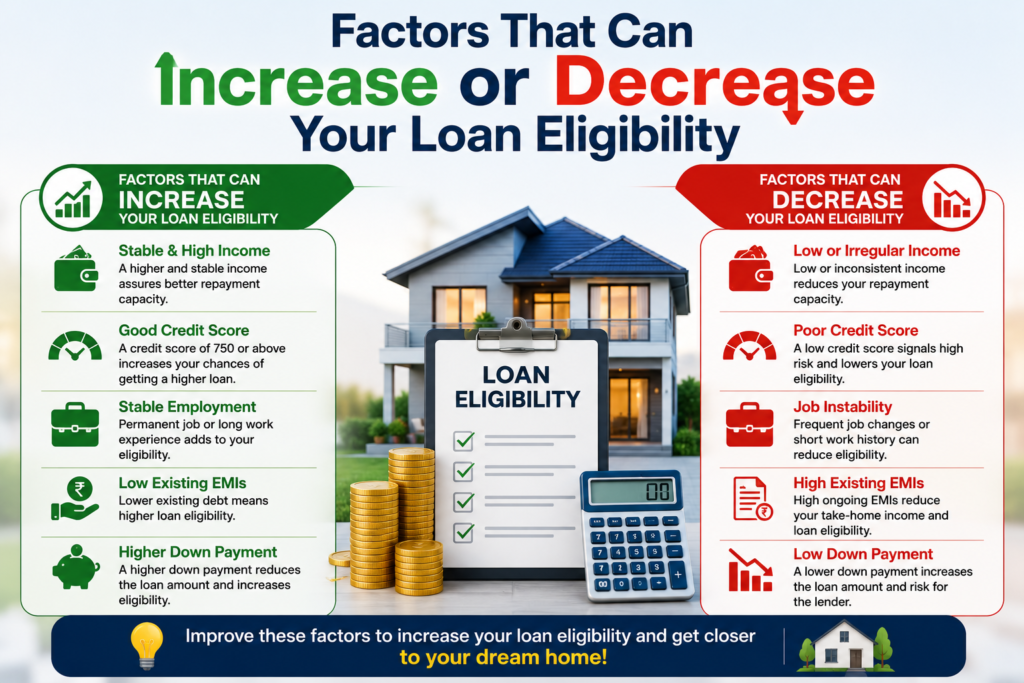

Factors That Can Increase or Decrease Your Loan Eligibility

Your approved loan amount is not decided only by your salary. Banks check several other factors before approval.

Credit Score

A good credit score increases your chances of getting better loan terms.

Benefits of a good credit score:

- Higher approval chances

- Better interest rates

- Smooth processing

Existing Loans

Existing EMIs reduce your disposable income.

For example:

Salary: ₹40,000

Existing EMI: ₹10,000

The bank will consider only the remaining income while calculating home loan eligibility.

Age of Applicant

Age affects loan tenure. Younger applicants may get longer repayment periods, which can increase eligibility.

Employment Stability

Banks prefer applicants with stable employment history.

Salaried employees with:

- Regular income

- Stable job

- Consistent salary records

usually have better chances of approval.

Home Loan Interest Rates and Their Impact on EMI

Choosing the right interest rate is important because a small change in rate can significantly affect total repayment.

Home loan interest rates in India are mainly of two types:

Floating Interest Rate

The interest rate changes according to market conditions.

Advantages:

- Possible benefit if rates decrease

- Usually preferred for long-term loans

Fixed Interest Rate

The interest rate remains fixed for a specific period.

Advantages:

- Predictable EMI

- Easier financial planning

Before choosing a bank, compare different lenders and check their current interest rates.

Borrowers who already have loans may need documents such as a HDFC home loan interest certificate to understand yearly interest payments and claim applicable tax benefits.

What Is Mortgage Loan Eligibility?

Mortgage loan eligibility refers to the criteria a lender uses to decide whether a person qualifies for a loan against property.

Factors considered include:

- Property value

- Applicant income

- Credit score

- Age

- Repayment capacity

Although home loans and mortgage loans are different, both require financial evaluation by the lender.

A person earning ₹40,000 salary should understand the difference between these loans before choosing the right financing option.

Can I Take a Home Renovation Loan on ₹40,000 Salary?

Apart from buying a house, many people require funds for repairing or improving their existing property.

A home renovation loan interest rate may differ from a regular home loan because it depends on the lender and loan type.

Home renovation loans can be used for:

- Kitchen renovation

- Bathroom upgrades

- Painting work

- Flooring

- Structural improvements

Eligibility depends on:

- Monthly income

- Property ownership

- Credit history

- Existing financial commitments

A person earning ₹40,000 salary may qualify for a renovation loan if they meet the bank’s criteria.

Using Bank-Specific Calculators Before Applying

Different banks provide online tools to help customers estimate their loan affordability.

For example:

- home loan eligibility calculator ICICI helps estimate eligibility based on income and repayment capacity.

- canara bank home loan emi calculator helps calculate expected monthly EMI before applying.

These tools are useful for financial planning but the final decision depends on document verification and bank approval.

Home Loan Eligibility Criteria for ₹40,000 Salary

Before approving a home loan, banks carefully evaluate the borrower’s financial condition. Even if you have a regular income of ₹40,000 per month, lenders check multiple factors to decide whether you are eligible for a loan.

Home loan eligibility for 40000 salary depends on:

- Monthly income

- Credit score

- Existing loans

- Age

- Employment stability

- Loan tenure

- Property value

- Repayment capacity

Banks want to ensure that the borrower can comfortably pay the EMI without facing financial difficulties. Therefore, salary is only one part of the eligibility assessment.

A person earning ₹40,000 monthly income can improve their chances of approval by maintaining a good credit history, reducing existing debts, and choosing a suitable loan amount.

Role of Credit Score in Home Loan Approval

Credit score is one of the most important factors considered during the home loan approval process.

A credit score represents your previous borrowing and repayment behavior. Banks use it to understand how responsibly you have managed your financial obligations.

Generally:

- 750+ score: Considered a strong credit profile

- 650–750 score: Approval depends on other factors

- Below 650: Loan approval may become difficult

A good credit score can help borrowers get:

- Faster loan approval

- Better interest rates

- Higher loan amount eligibility

- Better repayment terms

Before applying for a loan, check your credit report and clear any pending payments or outstanding debts.

Impact of Existing Loans on Home Loan Eligibility

Existing financial commitments directly affect your loan eligibility.

Banks calculate your repayment capacity after considering current EMIs.

For example:

Monthly Salary: ₹40,000

Existing EMI: ₹8,000

The bank will consider the remaining income while calculating your home loan eligibility.

Existing obligations may include:

- Personal loans

- Car loans

- Credit card payments

- Consumer loans

Reducing existing debt before applying can increase your chances of getting a higher loan amount.

Using a loan eligibility calculator can help you understand how your current financial commitments affect your borrowing capacity.

Importance of Age in Home Loan Eligibility

Age plays an important role because it determines the maximum repayment period available.

Banks usually prefer applicants who can complete repayment before retirement age.

For example:

A younger applicant may get:

- Longer loan tenure

- Lower EMI

- Higher loan eligibility

An older applicant may get:

- Shorter repayment period

- Higher EMI

- Lower eligible loan amount

Therefore, applying for a home loan at the right age can improve your borrowing capacity.

Employment Stability and Income Verification

Banks prefer borrowers who have stable employment and regular income.

For salaried employees, lenders usually check:

- Current employment duration

- Company profile

- Salary history

- Monthly bank credits

A person earning ₹40,000 salary with stable employment has better approval chances compared to someone with irregular income.

Self-employed applicants may need additional documents to prove business income and financial stability.

Down Payment Requirement for Home Loan

Down payment is the amount paid by the buyer from their own funds while purchasing a property.

Usually, banks finance a major portion of the property cost, while the remaining amount is paid by the buyer.

Example:

Property Price: ₹40 lakh

Bank Loan: ₹32 lakh

Buyer Contribution: ₹8 lakh

A higher down payment can provide several benefits:

- Lower loan amount

- Lower EMI

- Reduced interest burden

- Better approval chances

Before applying for a loan, plan your savings for down payment, registration charges, and other property-related expenses.

Documents Required for Home Loan on ₹40,000 Salary

Submitting the correct documents helps speed up the approval process.

Common documents required include:

Identity Proof

- Aadhaar Card

- PAN Card

- Passport

- Voter ID

Address Proof

- Aadhaar Card

- Electricity bill

- Passport

- Rental agreement (if applicable)

Income Proof for Salaried Employees

- Latest salary slips

- Bank statements

- Form 16

- Salary certificate

- Employment proof

Property Documents

- Sale agreement

- Property ownership documents

- Approved building plan

- Property tax receipts

Banks verify these documents before final loan approval.

Step-by-Step Home Loan Application Process

Applying for a home loan involves several steps:

Step 1: Check Eligibility

Before applying, calculate your approximate eligibility using a home loan eligibility calculator.

Check:

- Income

- EMI capacity

- Credit score

- Existing liabilities

Step 2: Compare Different Banks

Compare:

- Interest rates

- Processing fees

- Loan tenure

- Customer service

Different banks offer different loan terms, so selecting the right lender is important.

Step 3: Submit Application

Fill out the loan application form and submit required documents.

The bank reviews:

- Income details

- Credit history

- Employment information

Step 4: Property Verification

After initial approval, the bank checks the property documents and legal status.

Step 5: Loan Approval and Disbursement

After successful verification, the loan agreement is signed, and the approved amount is released according to the property purchase process.

Understanding Home Loan Pre Approval Process

Home loan pre approval is an initial approval given by a bank after checking your financial details.

During pre approval, the bank evaluates:

- Income

- Credit score

- Employment details

- Loan repayment capacity

Benefits of pre approval:

- Helps know your budget

- Makes property searching easier

- Improves negotiation power with sellers

- Saves processing time

However, final approval depends on property verification and legal checks.

How to Improve Home Loan Eligibility on ₹40,000 Salary

If your current eligibility is lower than expected, you can improve it by following these methods:

Improve Credit Score

Maintain timely payments and avoid unnecessary loan applications.

Reduce Existing Debts

Pay off small loans and credit card dues before applying.

Add a Co-Applicant

Adding a spouse or family member with income can increase total eligibility.

Choose Longer Tenure

A longer repayment period reduces EMI and may increase loan eligibility.

Increase Down Payment

A higher contribution reduces the required loan amount.

Maintain Stable Employment

Avoid frequent job changes before applying for a home loan.

Why Planning Before Applying for a Home Loan Is Important

Taking a home loan is a long-term financial commitment. A borrower should carefully analyze:

- Monthly income

- Future expenses

- EMI affordability

- Interest cost

- Emergency savings

Using tools like a home loan calculator, home loan eligibility calculator ICICI, and bank-specific EMI calculators can help borrowers make informed decisions.

Proper planning ensures that the loan supports your home ownership goal without creating unnecessary financial stress.

Best Banks for Home Loan on ₹40,000 Salary

Choosing the right bank is an important decision because a home loan is a long-term financial commitment. Different banks provide different interest rates, repayment options, processing charges, and customer services.

Before selecting a lender, borrowers should compare:

- Interest rates

- Loan tenure options

- Processing fees

- Prepayment rules

- Customer support

- Loan approval process

Some popular banks offering home loan services in India include:

State Bank of India (SBI) Home Loan

SBI is one of the largest public sector banks in India and provides home loans for different categories of borrowers. It offers various repayment options and competitive interest rates.

HDFC Home Loan

HDFC is known for housing finance services and provides home loans for purchasing, constructing, and renovating properties. Borrowers can also use documents like the HDFC home loan interest certificate for tracking annual interest payments and tax-related requirements.

ICICI Bank Home Loan

ICICI Bank provides digital loan services and online tools that help customers estimate their eligibility and EMI. Many users search for home loan eligibility calculator ICICI to get an approximate idea of their borrowing capacity before applying.

Canara Bank Home Loan

Canara Bank provides housing loan options for salaried and self-employed individuals. Customers can use tools like the canara bank home loan emi calculator to estimate their monthly repayment amount.

Before finalizing any bank, always compare the complete loan cost instead of only focusing on the interest rate.

Government Housing Schemes for Home Buyers

The Indian government has introduced various housing schemes to support people who want to purchase or construct homes.

Government housing programs focus on making affordable housing accessible to eligible citizens.

Some benefits may include:

- Financial assistance

- Subsidized interest benefits (where applicable)

- Support for affordable housing

Eligibility for government schemes depends on factors such as:

- Income category

- Location of property

- Applicant details

- Previous ownership status

- Government guidelines

People earning ₹40,000 monthly income should check the latest government rules before applying for any housing benefit.

Fixed vs Floating Home Loan Interest Rate: Which Is Better?

When selecting a home loan, borrowers usually choose between fixed and floating interest rates.

Fixed Interest Rate

In a fixed-rate loan, the interest rate remains unchanged for a specific period.

Advantages:

- Stable EMI payments

- Easier monthly budgeting

- Protection from market rate increases

Disadvantages:

- May have higher initial rates

- Limited benefit if market rates decrease

Floating Interest Rate

In a floating-rate loan, the interest rate changes according to market conditions.

Advantages:

- Possible benefit when interest rates decrease

- Often preferred for long-term loans

Disadvantages:

- EMI may increase when rates rise

Understanding home loan interest rates in India helps borrowers choose the right option according to their financial goals.

Common Mistakes to Avoid While Taking a Home Loan

Many borrowers make mistakes because they focus only on getting loan approval and ignore long-term financial planning.

1. Taking a Higher Loan Than Required

A higher loan amount means higher EMI and more interest payment. Always choose a loan amount that matches your repayment ability.

2. Ignoring Credit Score

A low credit score can reduce approval chances and may result in higher interest rates.

3. Not Comparing Different Banks

Different lenders offer different terms. Compare multiple banks before making a final decision.

4. Choosing the Wrong Tenure

A longer tenure reduces EMI but increases total interest payment. A shorter tenure saves interest but increases monthly burden.

5. Not Maintaining Emergency Savings

Before taking a home loan, maintain emergency funds for unexpected expenses.

How to Manage Home Loan EMI with ₹40,000 Salary

Managing EMI properly is important because a home loan continues for many years.

Some useful tips:

- Keep EMI within your comfortable income range

- Avoid unnecessary new loans

- Maintain emergency savings

- Increase income sources if possible

- Make part-prepayments whenever financially possible

Using a home loan calculator regularly can help track your repayment planning and understand future financial commitments.

CONCLUSION

Final Conclusion: Home Loan on ₹40,000 Salary

Getting a home loan on a ₹40,000 salary is possible with proper financial planning and a clear understanding of your financial position. Banks such as SBI evaluate multiple factors, including income, credit score, existing liabilities, age, employment stability, and repayment capacity before approving a home loan.

Before applying for a loan, borrowers should calculate their EMI using a home loan calculator, compare available loan options, understand home loan interest rates in India, and check their eligibility through a loan eligibility calculator.

A responsible approach includes maintaining a good credit score, arranging a sufficient down payment, selecting an affordable loan amount, and choosing a repayment tenure that matches your monthly budget. Comparing loan options from trusted lenders like SBI can help borrowers understand suitable interest rates, repayment plans, and loan features.

With proper planning, financial discipline, and the right loan strategy, a ₹40,000 monthly salary can become a strong foundation for achieving the goal of owning a home.

For More Update Click ON : https://www.loanspecialoffer.com/.

FAQ

No, most banks do not provide 100% financing for property purchases. Generally, borrowers need to arrange a certain percentage of the property cost as a down payment. The required amount depends on the bank’s policies, property value, and loan guidelines.

Yes, a fresher can apply for a home loan, but banks usually check employment stability, income consistency, and credit history. Applicants with a longer work experience may have better approval chances.

Yes, you can apply for a joint home loan with a spouse or eligible family member. Combining incomes may increase the total loan eligibility and improve approval chances.

Yes, frequent job changes may affect your loan approval because banks prefer applicants with stable employment. Maintaining consistent employment before applying can improve your profile.

In some cases, borrowers can request a loan enhancement or top-up loan after approval. The bank will review income, repayment history, credit score, and existing loan details before approving an additional amount.

The approval time depends on the lender, document verification, applicant profile, and property verification process. It may take anywhere from a few days to several weeks.

Yes, many borrowers choose part-prepayment or foreclosure to reduce their interest burden. However, prepayment rules may vary depending on the loan type and bank policies.

A low credit score can reduce approval chances, but rejection is not always guaranteed. Banks may consider other factors such as income, employment stability, loan amount, and repayment capacity.

Getting a home loan with cash salary can be difficult because banks generally require proper income proof such as salary slips, bank statements, and employment verification.

Yes, property location can affect approval. Banks check factors like property legality, market value, construction status, and approval documents before sanctioning the loan.

Disclaimer

The information provided in this article is for educational and informational purposes only. Home loan eligibility, loan amount, interest rates, EMI calculations, and approval criteria may vary depending on the bank, lender policies, credit score, income, employment profile, loan tenure, and other financial factors. The estimated calculations mentioned in this article are only for general understanding and should not be considered as financial advice. Before applying for any home loan, readers are advised to check the latest terms and conditions with the respective bank or consult a qualified financial advisor