Applying for a personal loan has become much easier than it was a few years ago. Instead of visiting multiple bank branches, filling out lengthy paper forms, and waiting several days for approval, many borrowers now prefer digital lending platforms that allow them to complete the entire process online. Among these, Paytm Personal Loan has become one of the most searched borrowing options because eligible users can check loan offers directly through the Paytm app, which works with RBI-regulated banks and NBFCs.However, getting approved isn’t as simple as downloading an app and clicking the Apply button. Every lending partner follows its own eligibility checks, verifies your financial profile, reviews your credit history, and evaluates your repayment capacity before sanctioning a loan. Understanding these requirements beforehand can significantly improve your chances of approval while helping you avoid unnecessary loan rejections.

In this detailed guide, you’ll learn everything you need to know—from Paytm loan eligibility, interest rates, required documents, repayment options, approval factors, common mistakes to avoid, and practical tips that can help you borrow responsibly in 2026.

Important: Paytm itself is not a bank. Personal loans available through the Paytm app are offered by RBI-regulated banks and Non-Banking Financial Companies (NBFCs), subject to their individual lending policies and eligibility criteria.

What is Paytm Personal Loan?

A Paytm Personal Loan is an unsecured digital loan that eligible users can access through the Paytm app. Since it is an unsecured credit facility, borrowers are not required to pledge assets such as gold, property, or vehicles as collateral. Instead, lending decisions are primarily based on factors like income, employment stability, repayment history, credit score, and overall financial health.

Unlike traditional bank loans that often require branch visits and manual verification, digital lenders streamline the application process using online KYC verification, automated document checks, and digital underwriting. Once approved, the sanctioned loan amount is usually transferred directly to the applicant’s registered bank account.It is important to understand that Paytm acts as a technology platform connecting users with authorized lending partners. The actual loan agreement, applicable interest rate, repayment tenure, processing charges, and approval decision are determined entirely by the respective bank or NBFC.

Paytm Personal Loan at a Glance

| Feature | Details |

| Loan Type | Unsecured Personal Loan |

| Application Mode | 100% Online |

| Collateral Required | No |

| Available Through | Paytm App |

| Lending Partners | RBI-Regulated Banks & NBFCs |

| Disbursement | Direct Bank Transfer (after approval) |

| Best For | Medical expenses, education, travel, home renovation, emergencies, debt consolidation and other personal needs |

| Repayment Mode | Monthly EMI |

| Identity Verification | Digital KYC |

Note: Loan amount, tenure, eligibility, and interest rates vary depending on the lending partner and the applicant’s credit profile.

Why More Borrowers Prefer Digital Personal Loans

The popularity of digital lending has increased because borrowers now expect faster services without unnecessary paperwork. Instead of waiting several days for document verification, applicants can upload their KYC documents digitally and receive updates directly through the app.

Another major advantage is convenience. Whether you’re applying from home, your workplace, or while travelling, the entire application process can usually be completed using a smartphone with an internet connection. This eliminates the need for repeated branch visits and makes borrowing more accessible for eligible individuals across different cities.

Digital lending platforms also provide greater transparency. Applicants can generally review the offered loan amount, applicable charges, repayment schedule, and monthly EMI before accepting the final loan agreement, allowing them to make informed financial decisions.

Key Features of Paytm Instant Personal Loan

The growing demand for Paytm instant personal loan services is driven by speed, convenience, and a simplified application experience. While approval is always subject to the lending partner’s assessment, eligible borrowers can benefit from several useful features.

Some of the key advantages include:

- Fully digital application process

- No collateral or security required

- Paperless document submission

- Online KYC verification

- Flexible repayment options

- Transparent loan agreement

- Direct transfer of approved loan amount

- Real-time application status tracking

- Multiple RBI-regulated lending partners available through the platform

These features make digital lending especially useful for individuals who need quick financial assistance without completing lengthy offline procedures.

Is Paytm Personal Loan Safe?

One of the most common questions borrowers ask is whether applying through Paytm is safe.

The answer depends on understanding how the platform works. Paytm itself facilitates the loan application process by connecting eligible users with regulated financial institutions. The actual loan is provided by RBI-authorized banks or NBFCs that follow applicable lending regulations, digital KYC requirements, and customer verification procedures.

Before accepting any loan offer, borrowers should always review:

- Interest rate

- Processing charges

- Repayment tenure

- Foreclosure conditions

- Late payment penalties

- Total repayment amount

Reading the complete loan agreement before accepting the offer helps prevent unexpected charges later.

Who Can Apply for a Paytm Personal Loan?

Although eligibility varies between different lending partners, personal loans are generally available to individuals who demonstrate a stable financial profile and sufficient repayment capacity.

Applicants commonly include:

- Salaried employees

- Self-employed professionals

- Business owners

- Freelancers (where accepted by the lender)

- Professionals with regular income

Simply meeting the minimum eligibility conditions does not guarantee approval. Lenders evaluate several financial indicators before making a final decision.

Basic Paytm Loan Eligibility Criteria

Before submitting your application, it’s helpful to understand the common Paytm loan eligibility requirements followed by most lending partners.

| Eligibility Factor | General Requirement |

| Citizenship | Indian Resident |

| Age | As per lender policy |

| Income | Stable and verifiable income |

| Employment | Salaried or self-employed (depending on lender) |

| Credit History | Good repayment behaviour preferred |

| Bank Account | Active bank account |

| PAN Card | Mandatory for verification |

| KYC | Identity verification required |

Different banks and NBFCs may introduce additional eligibility requirements depending on their internal risk assessment models.

Factors That Affect Loan Approval

Loan approval is based on much more than income alone. Modern digital lenders evaluate an applicant’s overall financial profile before deciding whether to sanction a personal loan.

Some of the most important factors include:

1. Credit Score

A healthy credit score reflects responsible borrowing behaviour and timely repayment of previous loans or credit card bills. Higher scores generally improve approval chances and may also help borrowers receive better loan terms.

2. Monthly Income

Lenders assess whether your regular income is sufficient to comfortably repay the proposed EMI without creating financial stress.

3. Existing Financial Obligations

If a significant portion of your income is already committed to existing EMIs or credit card payments, lenders may consider your repayment capacity lower.

4. Employment Stability

Applicants with a consistent employment history or stable business income are generally viewed as lower-risk borrowers.

5. Credit History

Apart from the credit score itself, lenders also review repayment behaviour, previous loan defaults, delayed payments, loan settlements, and overall credit discipline.

6. Digital Verification

Accurate KYC details, valid PAN information, readable documents, and successful verification contribute to a smoother approval process.

Interest Rate, Processing Fees & Other Charges

One of the biggest mistakes borrowers make is focusing only on the approved loan amount while overlooking the total borrowing cost. Besides the interest rate, lenders may also charge processing fees, GST, late payment penalties, bounce charges, or foreclosure fees. Understanding these costs beforehand helps you compare loan offers more effectively and prevents unexpected expenses later.

The Paytm loan interest rate is not fixed for every applicant. Since loans are offered by different RBI-regulated banks and NBFCs, each lender follows its own pricing model. Factors such as your credit score, monthly income, employment stability, repayment history, loan amount, and repayment tenure all influence the final rate offered.

Common Charges You Should Review

| Charge | What It Means |

| Interest Rate | Annual cost charged on the borrowed amount |

| Processing Fee | One-time fee deducted before disbursement or charged separately |

| GST | Applicable on processing fees and certain service charges |

| Late Payment Charges | Penalty for missing EMI due dates |

| EMI Bounce Charges | Applicable if auto-debit fails |

| Foreclosure Charges | May apply if you repay the loan before completion |

| Part-Payment Charges | Some lenders charge for partial prepayments |

Expert Tip: Never compare loans based only on interest rates. Always compare the total repayment amount, processing fee, tenure, and additional charges before accepting any offer.

Paytm Personal Loan Documents Required

Keeping your documents ready before applying can significantly speed up verification and reduce delays. Although requirements differ slightly among lending partners, most lenders ask for standard KYC and income-related documents.

Having clear and updated copies of the Paytm personal loan documents required also improves the chances of smooth verification, especially during digital KYC.

Documents Commonly Required

| Document | Purpose |

| PAN Card | Identity and tax verification |

| Aadhaar Card or other valid ID | Identity verification |

| Address Proof | Residential verification |

| Passport-size Photograph | Applicant identification |

| Salary Slips (Salaried Applicants) | Income proof |

| Bank Statements | Income and transaction history |

| Income Tax Returns (Self-employed) | Business income verification |

| Business Proof (if applicable) | Verification for self-employed applicants |

Tips Before Uploading Documents

- Upload high-quality scanned copies or clear photographs.

- Ensure your PAN details match your bank records.

- Use your latest salary slips or recent bank statements.

- Avoid uploading cropped, blurred, or incomplete documents.

- Verify that your registered mobile number is active for OTP verification.

Step-by-Step Guide to Apply Online

The Paytm loan online apply process is designed to be simple, but entering accurate information at every stage is important. Incorrect details or incomplete documentation can delay approval or even lead to rejection.

Application Process

- Open the Paytm app.

- Navigate to the Loans or Financial Services section.

- Check whether a loan offer is available for your profile.

- Complete your digital KYC verification.

- Fill in your personal, employment, and income details.

- Upload the required documents.

- Review the loan amount, interest rate, tenure, and charges.

- Accept the lender’s terms and conditions.

- Wait for verification and credit assessment.

- If approved, the sanctioned amount is transferred directly to your registered bank account.

Important: Receiving a pre-approved offer does not always guarantee final disbursement. The lender may still complete additional verification before approving the loan.

How Long Does Loan Approval Usually Take?

Many applicants expect immediate approval after submitting an application. In reality, approval time depends on document verification, KYC completion, lender policies, and the applicant’s financial profile.

If all submitted information is accurate and verification is completed successfully, digital lenders may process eligible applications much faster than traditional offline loans. However, additional verification may increase the overall processing time.

Factors Affecting Processing Time

- Accuracy of submitted documents

- Successful digital KYC verification

- Credit history review

- Income verification

- Existing loan obligations

- Internal lender approval process

Keeping all documents ready and providing accurate information helps reduce unnecessary delays.

Common Reasons Personal Loan Applications Get Rejected

Loan rejection doesn’t always indicate poor financial health. In many cases, applications are declined because of avoidable mistakes made during the application process.

Understanding these common reasons can help you prepare better before applying.

Major Reasons for Rejection

| Reason | Impact |

| Low Credit Score | Higher lending risk |

| Insufficient Income | Lower repayment capacity |

| High Existing EMIs | Increased debt burden |

| Incorrect Personal Details | Verification failure |

| Poor Credit History | Missed payments or loan defaults |

| Multiple Loan Applications | Multiple hard inquiries on credit report |

| Incomplete Documents | Delayed or failed verification |

| Mismatch in KYC Details | Identity verification issues |

How to Improve Your Approval Chances

Getting approved isn’t only about earning a high salary. Lenders assess your overall financial discipline, repayment behaviour, and ability to manage future EMIs responsibly.

Following a few practical habits before applying can significantly strengthen your application.

Best Practices Before Applying

- Check your credit report for errors.

- Pay existing EMIs and credit card bills on time.

- Avoid applying with multiple lenders simultaneously.

- Keep your debt-to-income ratio under control.

- Maintain a stable source of income.

- Upload accurate and readable documents.

- Use the same mobile number linked with your bank and KYC records.

- Apply only for the amount you genuinely require.

These simple steps demonstrate responsible borrowing behaviour and may improve lender confidence during credit assessment.

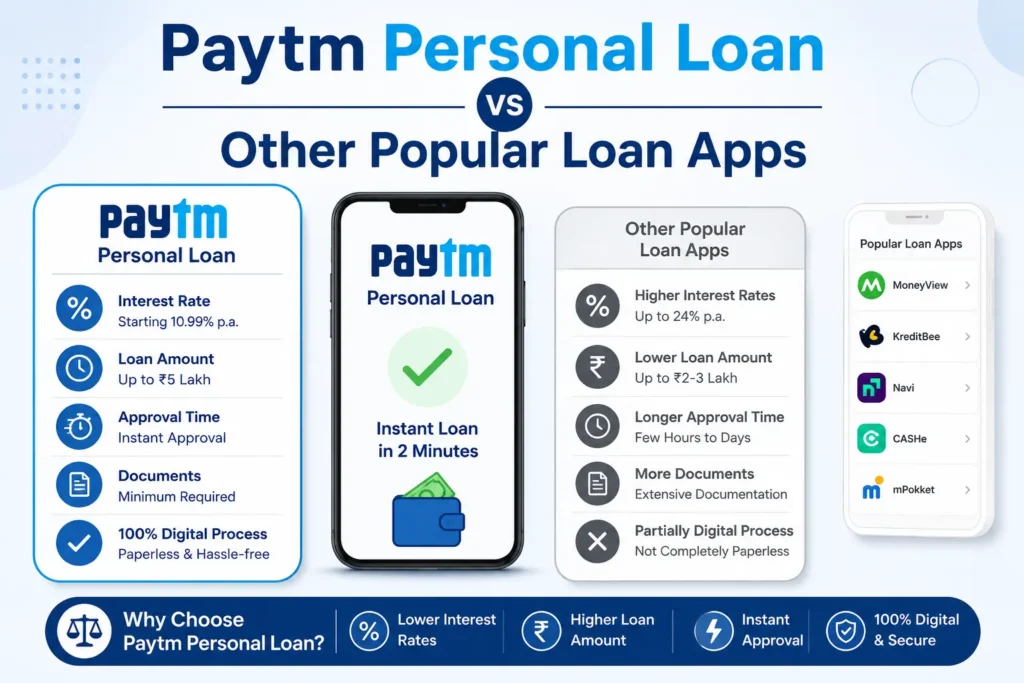

Paytm Personal Loan vs Other Popular Loan Apps

Many borrowers compare multiple platforms before making a final decision. Instead of choosing the first available offer, compare eligibility, repayment flexibility, interest rates, charges, and customer support.

| Feature | Paytm | Traditional Bank | Digital Loan Apps |

| Online Application | Yes | Limited (depends on bank) | Yes |

| Paperless Process | Yes | Often partial | Mostly Yes |

| Branch Visit | Usually No | Often Required | Usually No |

| Multiple Lending Partners | Yes | No | Depends on platform |

| Digital KYC | Yes | Available in many banks | Yes |

| Loan Tracking | Yes | Varies | Yes |

Rather than selecting a lender solely because of faster processing, evaluate the complete borrowing cost, repayment flexibility, and transparency of terms. A loan with a slightly lower interest rate but higher hidden charges may end up costing more over time.

Personal Loan Repayment Options & Choosing the Right Loan Tenure

Selecting the right repayment period is just as important as choosing the loan amount. Many borrowers focus only on getting quick approval, but the repayment tenure directly affects both your monthly EMI and the total interest you pay over the life of the loan.

A longer personal loan maximum tenure generally reduces your monthly EMI, making repayments easier to manage. However, because interest is charged for a longer duration, the overall borrowing cost increases. On the other hand, a shorter repayment period results in higher EMIs but helps you become debt-free sooner while reducing the total interest paid.

How Different Loan Tenures Affect Your Repayment

| Loan Tenure | Monthly EMI | Total Interest Paid | Suitable For |

| Short Tenure | Higher | Lower | Borrowers with stable income |

| Medium Tenure | Moderate | Moderate | Balanced repayment planning |

| Long Tenure | Lower | Higher | Those needing lower monthly EMIs |

The ideal tenure depends on your income, financial commitments, and monthly budget. Choosing an EMI that comfortably fits your finances is usually better than selecting the longest repayment period available.

When Should You Consider Short-Term Loans?

There are situations where short term loans can be a practical financial solution. They are generally suitable for temporary cash-flow requirements rather than long-term financial commitments.

Examples include:

- Medical emergencies

- Unexpected home repairs

- Education-related expenses

- Wedding expenses

- Temporary business cash requirements

- Urgent travel needs

Before borrowing, always evaluate whether the monthly EMI fits comfortably within your income. Borrowing beyond your repayment capacity may affect your future credit profile.

Advantages and Limitations of Paytm Personal Loan

Every financial product has both benefits and limitations. Understanding both sides helps borrowers make informed decisions rather than choosing a loan based only on advertisements or approval speed.

Advantages

- Fully digital application process

- No collateral required

- Convenient online document submission

- Digital KYC verification

- Transparent EMI schedule

- Access to multiple RBI-regulated lending partners

- Suitable for various personal financial needs

- Easy application tracking through the app

Limitations

- Approval depends on lender eligibility criteria.

- Credit score plays an important role.

- Interest rates differ between applicants.

- Processing fees and additional charges may apply.

- Not every Paytm user receives a loan offer.

- Loan amount and tenure vary according to financial profile.

Important Things to Check Before Accepting Any Loan Offer

Receiving a loan offer does not necessarily mean you should accept it immediately. Taking a few extra minutes to review the complete loan agreement can help you avoid unnecessary costs later.

Before accepting any offer, carefully verify the following:

| Checklist | Why It Matters |

| Approved Loan Amount | Ensure it matches your requirement |

| Interest Rate | Understand the total borrowing cost |

| EMI Amount | Confirm it fits your monthly budget |

| Repayment Tenure | Choose a comfortable repayment period |

| Processing Fee | Know the upfront charges |

| GST & Other Charges | Check applicable taxes and fees |

| Late Payment Charges | Understand penalty terms |

| Foreclosure Policy | Review conditions for early repayment |

| Total Repayment Amount | Calculate overall financial commitment |

Never rely solely on promotional advertisements. Reading the official loan agreement carefully is one of the most important steps before borrowing.

Responsible Borrowing Practices

A personal loan should be used thoughtfully and only when it genuinely supports an important financial requirement. While digital lending has made borrowing faster and more accessible, responsible repayment remains the borrower’s responsibility.

Financial experts generally recommend borrowing only the amount you actually need instead of accepting the maximum amount offered. Keeping your monthly EMI within a manageable portion of your income reduces financial stress and lowers the risk of missed payments.Maintaining timely repayments also contributes to a healthy credit history, which may improve your eligibility for future financial products.

Expert Tips Before Applying

Following a few simple practices before submitting your application can improve your borrowing experience.

Financial Planning Tips

- Compare offers from different eligible lenders.

- Review all applicable charges—not just the interest rate.

- Check your credit report before applying.

- Keep all KYC documents updated.

- Avoid applying for multiple loans within a short period.

- Borrow only what you genuinely require.

- Ensure sufficient balance for automatic EMI deductions.

- Read every term and condition before accepting the agreement.

Small financial decisions made before borrowing often have a significant impact on your long-term financial health.

Key Takeaways

- Personal loans available through Paytm are offered by RBI-regulated banks and NBFCs.

- Approval depends on factors such as income, repayment history, employment stability, and credit profile.

- Comparing the total borrowing cost is more important than comparing only interest rates.

- Always verify eligibility before applying.

- Keep all documents ready to avoid processing delays.

- Read the complete loan agreement before accepting any offer.

- Borrow responsibly and choose a repayment tenure that suits your monthly budget.

Conclusion

A Paytm Personal Loan can be a convenient financing option for eligible borrowers seeking a fully digital borrowing experience. Since loans are provided by RBI regulated banks and NBFCs through the Paytm platform, approval depends on the lending partner’s evaluation of your financial profile rather than simply submitting an online application.

Before applying, compare available offers, review the eligibility criteria, understand the interest rate and applicable charges, and ensure that the monthly EMI comfortably fits your budget. Taking the time to verify these details can help you make a more informed borrowing decision.Most importantly, treat a personal loan as a financial responsibility rather than additional income. Borrow only when necessary, repay every EMI on time, and maintain healthy credit habits to strengthen your financial profile for future borrowing needs.

Disclaimer: Loan amounts, interest rates, repayment tenures, processing fees, and eligibility requirements may change over time and differ across lending partners. Always refer to the latest terms and conditions provided by the respective bank or NBFC before applying.

(FAQ)

No. Paytm acts as a digital platform that connects eligible users with RBI-regulated banks and NBFCs. The lending partner makes the final decision regarding loan approval, interest rates, repayment terms, and disbursement.

Maintaining a healthy credit score, stable income, timely repayment history, accurate KYC documents, and a reasonable debt-to-income ratio generally improves your chances of receiving loan approval.

Yes. Many lending partners also provide personal loans to self-employed professionals and business owners, provided they satisfy the lender’s income, documentation, and eligibility requirements.

Yes. Every formal loan application may generate a hard inquiry on your credit report. Submitting multiple applications within a short period can negatively impact your credit profile.

Many lenders allow prepayment or foreclosure of personal loans. However, some may charge foreclosure or part-payment fees, so reviewing the loan agreement beforehand is advisable.

Missing an EMI may lead to late payment charges, additional interest, and a negative impact on your credit history. Repeated defaults can also affect future borrowing eligibility.

No. Personal loans offered through Paytm’s lending partners are generally unsecured loans, which means collateral such as property, gold, or vehicles is usually not required.

Yes. Applicants can generally monitor the status of their loan application through the Paytm app during different stages of verification and approval.

A stronger credit score generally improves approval chances and may help borrowers receive more favourable loan terms. However, lenders also evaluate income, employment stability, repayment capacity, and other financial factors.

Leave a Reply