The credit score, the master key to every loan, basically dictates our level of responsibility and more importantly, the interest rate we pay on loans. However, this increasing dependence on credit score by the Indian financial system is coming under fire regarding its accuracy, accountability and transparency and has come to the point of power being wielded by the regulatory authorities (regulated banking system) over individual consumer rights. As has been quoted,

“Your financial identity is now reduced to a three digit number”.

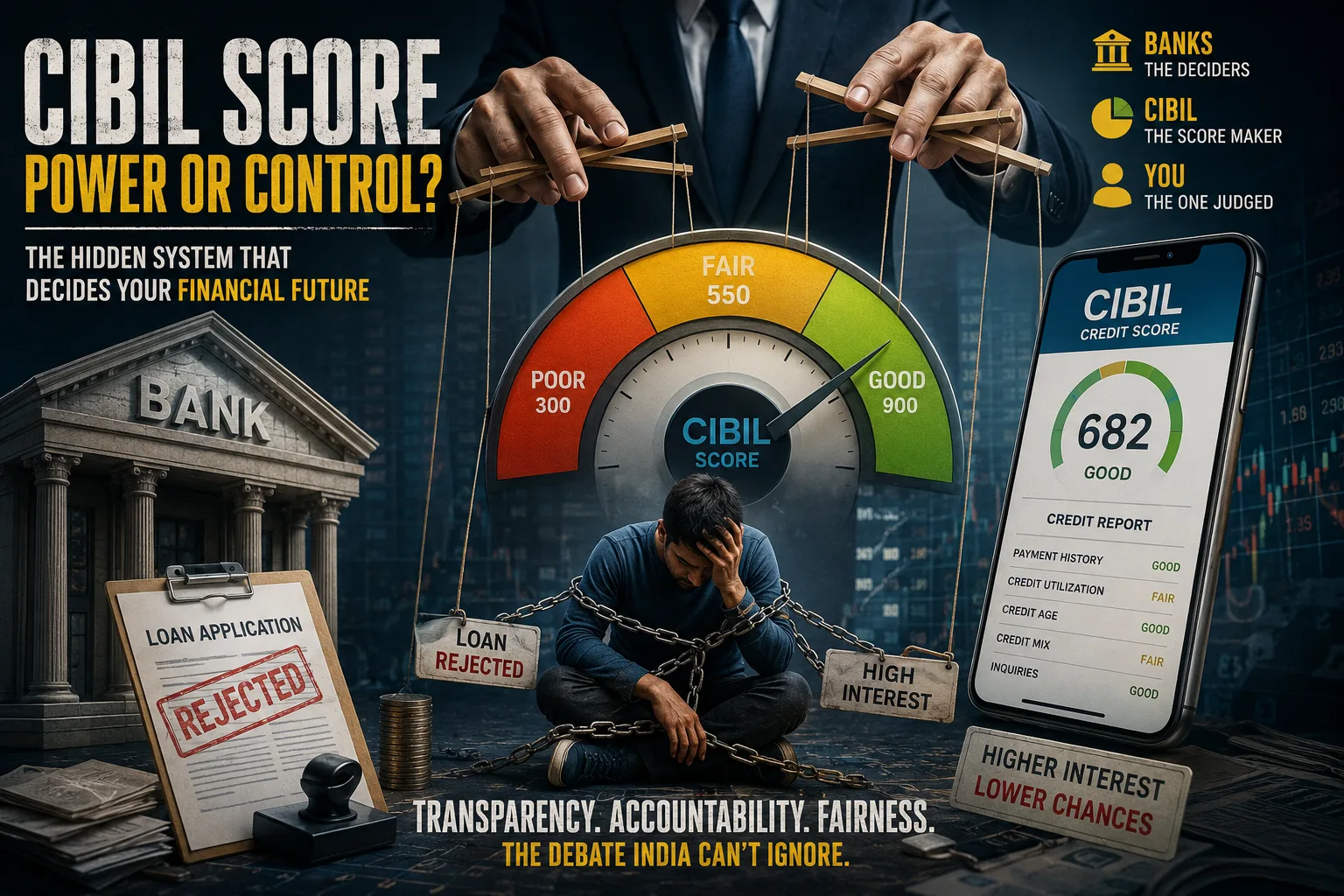

What is CIBIL and why should I care?

Credit Information Bureau India Limited, also known as CIBIL, is India’s first and foremost credit bureau, which is also a subsidiary completely owned by Trans Union CIBIL. It has consolidated the personal and private credit financial dealings carried out between consumers, credit card companies, banks and non-banking finance institutions. The financial dealings carried out have been converted into a score based on the repayment pattern (typically ranging from 300-900). This score is instrumental in processing your loan, determining your interest rate, eligibility for credit cards and more significantly to know your level of credit-worthiness in the market.

“A three digit score to prove your financial credit-worthiness.”

Core Public Issue: The Transparency Problem

No one debates on the discontinuance of credit scores, the problem really lies in the way they work without anyone knowing their mechanism. Individuals are now subject to a sudden drop in their credit score, banks providing inaccurate reports based on inflated and false data, a lengthy process of reflecting repayments, inability of banks to justify the score, slow pace in error correction and complaint filling.

“You are judged, but no one tells you why or how”.

Political Issue in India

A Lok Sabha member and a staunch critic of the credit bureaus Mr Karti P. Chidambaram questioned the credit score system based on its opaqueness, ignorance on part of consumers about the entire system, the high number of inaccurate reports affecting loan approvals and complete over-dependence on the credit scores by banks.

“System is not visible but it has the key to access your financial assets”.

Government’s stance

The government does not aim to ban credit bureaus, but instead to strengthen the existing financial regulatory system. The “credit bureaus are essential in modern banking, however, a person with no credit history should not be rejected on a loan application and your credit worthiness should not depend solely on the score. The capacity of an individual on repayment should be taken into account along with income”, according to the government. ‘System must be reformed, not removed.’

What was the official statement from CIBIL?

CIBIL stated that it works on data provided by banks, non-banking finance institutions and credit card companies, therefore it has nothing to do in either modifying or verifying the repayments as received. All errors are to be blamed on the erroneous data passed on by the financial institutions. They further stated that individuals should file dispute regarding any erroneous information given.

Famous CIBIL statements:

- We are a data repository and not a decision maker

- We have members like banks who provide data

- we can only do what they say

- consumers should raise disputes to correct them

- We have a RBI guided operational process

- We do not create the data, we only present it.

The role of banks and structural power

Banks consider a credit score as a reliable, quick and scalable source of risk assessment of an individual’s credit-worthiness. With numerous loans to process daily, credit scores come in as an effective medium of understanding the entire loan proposal to help banks increase their loan processing capacity, effectively manage loan risks as they have a strong scoring parameter to decide whom to approve the loan to, and a measure of control for those with good credit scores. However, banks are also criticized for their excessive reliance on the scores, automation, complete negation of human review process and a sharp increase in the interest rate for the consumers.

“Banks decide if they want to provide you access; CIBIL decides if you are eligible for that.”

RBI regulations

India’s credit bureaus have been brought under a set regulatory framework under the Credit Information Companies (Regulation) Act, 2005. Several reforms are brought in to improve efficiency including the mandates of one free credit report annually by the banks, setting timelines for the update of credit data, introducing a complaint redressal system and penalties to be levied on the banks for inaccurate reports.

“The government and RBI are moving toward tighter regulations”.

Recent changes

New policies formulated by the government and the RBI aim to quickly update financial reports and implement real-time credit reporting systems. This policy aims to increase accountability of banks and NBFCs to their clients.

“A future is coming where credit reports will be updated real-time”.

Has anyone demanded a ban on CIBIL?

To date, there have been no substantial efforts to impose a ban on CIBIL thanks to its significant role in managing financial stability, risk assessment and prevention of financial frauds in the country.

“The system can be changed, not destroyed.”

Real Debate: Whose financial identity is it?

The issue lies not in the existence of CIBIL, but its modus operandi. Who owns my financial information? What is the methodology to calculate a credit score? How timely can any discrepancies be rectified? What is the level of banks’ involvement in the process? What are the rights an individual holds?

“Who truly controls your financial identity?”.

The Algorithmic Cage: How Parliament is Challenging CIBIL’s Financial Monopoly

As highlighted in coverage by The Economic Times, the structural power of credit bureaus has faced unprecedented scrutiny at the highest legislative levels. Reports detailing the recent parliamentary debates—specifically the interventions by Lok Sabha MP Karti Chidambaram—underscore a growing political concern that an individual’s financial identity is effectively trapped in an opaque, automated scoring system. The Economic Times noted that this top-down pressure has magnified public demand for absolute transparency, challenging the unchallenged status of CIBIL and forcing both regulators and financial institutions to reconsider how algorithmic credit scores dictate financial access for millions of Indians.

Conclusion

The credit score system used by CIBIL is the backbone of the Indian banking industry as it facilitates a speedy loan approval process. However, issues like data accuracy, inflated credit scores and lack of transparency have attracted severe criticism from political leaders like Karti P. Chidambaram, pushing the RBI to reinforce regulations over credit bureaus. The primary intention of the government and the RBI is to introduce improved and more transparent credit score systems and strengthen the regulatory measures further.

“The solution lies in reformation, not abolishment”.